November 27, 2023 | Article by Chain | Cohn | Clark staff Social Share

After a car accident, there’s a flurry of activity. The paramedics come to care for those who are injured. The police assess the situation and make a report. You exchange information with other drivers. A tow truck hauls your damaged car off to a repair shop—and then it hits you: How am I going to get around? How will I get to work? Who’s going to pick up my kids from school?

The good news is that, yes—there are multiple ways to get insurance to pay for a rental car while your vehicle is being repaired. The not-so-good news is that some of these scenarios can be messy and confusing.

Let’s take a closer look.

Rental Car Coverage in an Accident When You’re Not at Fault

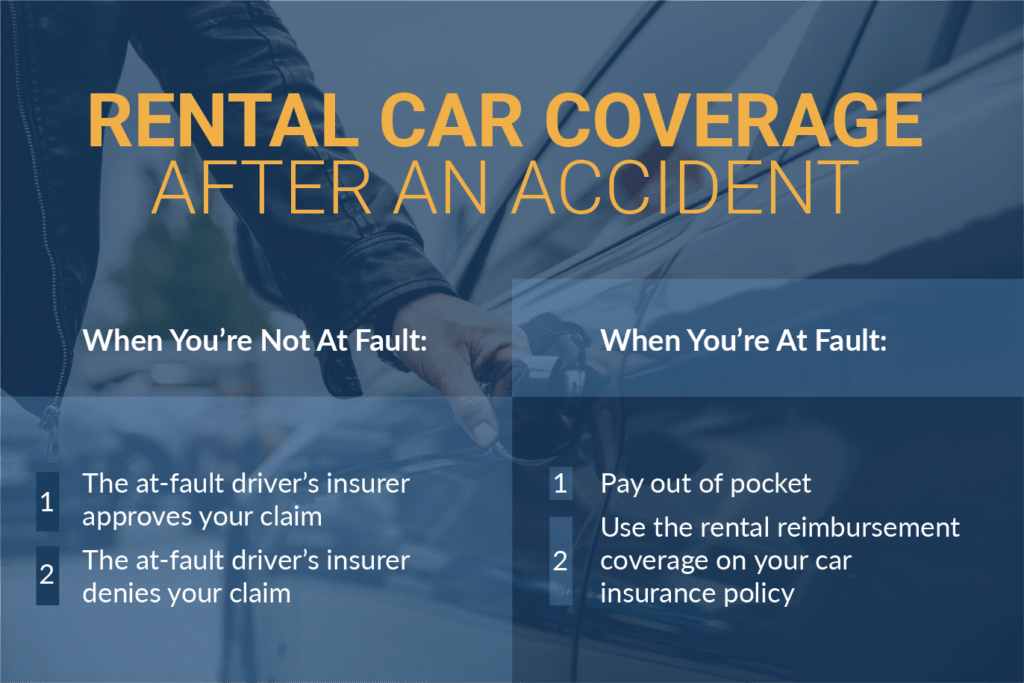

How do you get a rental car from an insurance claim? If you’re not at fault in an accident, the process is simple: file a claim with the at-fault driver’s insurance company asking for rental car coverage while your own vehicle is unavailable.

After you file a claim, there are two ways events may play out:

- The at-fault driver’s insurer approves your claim: In this scenario, you have a green light to rent a car while yours is being repaired or you’re waiting for a payout for a totaled vehicle. Stay within the limitations stipulated by the insurance company (e.g., a daily maximum rental charge) to avoid being hit with out-of-pocket costs.

- The at-fault driver’s insurer denies your claim: In this scenario, you don’t have any insurance coverage for a rental car. Insurance companies usually deny this type of claim when there’s a question regarding who was to blame for the accident or as a delaying tactic. You can dispute the denial of your claim, but the dispute process will take some time. If you need a car in the meantime, you can either pay for it yourself or use the rental reimbursement coverage on your own car insurance policy—if you have it. (See below for more information on rental reimbursement coverage.)

Rental Car Coverage in an Accident When You’re at Fault

In a state that uses fault to determine financial responsibility after a car accident (like California), the at-fault driver (or their insurance company) pays for rental car costs.

So, if you’re at fault in an accident and need a rental car while yours is in the shop, you’re on the hook for rental car charges. There are two ways to handle the cost:

- Pay out of pocket.

- Use the rental reimbursement coverage on your car insurance policy—if you have it. (See below for more information on rental reimbursement coverage.)

How Does Rental Reimbursement Insurance Work?

Rental reimbursement insurance goes by a few names. The most common is rental reimbursement insurance, but it’s sometimes called rental car coverage or extended transportation expenses.

Rental reimbursement insurance is an optional coverage—it’s your choice whether to add it to your policy. It covers you when there’s an incident that’s covered under two other optional coverages: comprehensive and collision.

- Comprehensive pays for uncontrollable events, like a tree falling on your car or hail damage.

- Collision pays for damage to your car and its contents if you hit a stationary object (e.g., a tree) or if you’re in a collision with another vehicle—no matter who’s at fault.

Rental reimbursement coverage is often very inexpensive—as little as $1 per month—but you may need to add comprehensive and/or collision to your policy before it’s available.

How Does Rental Reimbursement Coverage Work?

If an incident falls under your collision or comprehensive coverage, you can file a claim for rental car expenses. Policies vary, but most have the following features:

- A daily limit: This is the maximum a policy will pay each day toward a rental car. Amounts vary widely, so check your policy for the amount that applies to you. If you spend more than the daily limit, you must pay the difference. For example, if your daily coverage is $40, and you rent a car for $50 per day, you must pay the excess ($10) yourself.

- A per-incident limit: This refers to either the maximum dollar amount (e.g., $1,000) or the maximum number of days (e.g., 30 days) of coverage for any given accident.

Many policies stipulate that coverage only applies to the daily rental charge; this means that any extras—such as damage waivers—are not included. Some policies cover public transit costs as an alternative to renting a car.

If your policy has a per-incident dollar limit, you can stretch out your coverage over a longer time period by renting a cheaper car.

Some insurance companies have preferred rental car companies. If you rent from a preferred company, the insurance company may pay for the rental directly—in other words, you won’t have to pay out of pocket and wait to get reimbursed. Other insurance companies consider car rental a “paid when incurred” item. “Paid when incurred” means you only receive insurance money for a car rental after you pay for it and submit a receipt to the insurance company. An accident lawyer in Bakersfield can help if you’re struggling with your claim.

Bakersfield Personal Injury Attorneys

If you don’t have a car to drive because of an accident caused by another driver, your rental costs should be covered. But often, a claim for rental car coverage doesn’t work out in a straightforward way. If you’re struggling with navigating an insurance claim after a car accident, you may benefit from legal representation. Chain | Cohn | Clark’s experienced personal injury lawyers can take the load off your shoulders and help you get the compensation you deserve.

For a free, no-obligation review of your case, contact us today.