What’s the Average Car Accident Settlement in Bakersfield, California?

At Chain | Cohn | Clark, we have a team of experienced Bakersfield car accident lawyers, and we get it—everyone wants to know what their car accident claim is worth. We hear these questions all the time:

- What’s the average settlement for a non-injury car accident?

- What’s a typical car accident settlement amount when there are injuries?

- How much money can I expect from my car accident settlement?

You may not find our answers very satisfying, but we have to be truthful.

First, there aren’t accurate, systematic estimates for an “average” car accident settlement in California (or anywhere else, for that matter). Second, other websites may give you average settlement amounts—but we urge you not to trust those estimates.

What we can tell you is that each car accident is unique, and settlement amounts are influenced by many factors—factors we’ll cover in this blog. Settlement amounts are affected by whether or not there were injuries in an accident. And the location of an accident—for example, in Bakersfield, California—does affect the settlement amount.

Over the years, we’ve accumulated a track record of substantial case results, but it’s important to realize that each case is unique. The best way to get an idea of what your car accident claim might be worth is to contact a car accident law firm like Chain | Cohn | Clark for a free consultation.

To learn more about the factors that influence the amount of a car accident settlement in Bakersfield, keep reading.

Car Accident Basics

If you want to understand what influences the amount of a car accident settlement, you need to understand some basic car accident–related topics.

What to Do After a Car Accident in California

What you do in the immediate aftermath of a car accident and in the days and weeks that follow is one of the strongest influences on your car accident settlement—aside from the particulars of the accident itself.

Here’s a brief list of things to do after a car accident (we provided a detailed list of what to do after a car accident in a previous blog article):

- Call 911 to get first responders on the scene.

- Collect contact and insurance from everyone involved in the accident.

- Report the accident to the local police department and the Department of Motor Vehicles (DMV) if there is more than $1,000 in property damage or if someone is injured.

- Get a copy of the police report for the accident.

- Get contact information for any witnesses to the accident.

- Take photos or videos of the accident scene. Include vehicle damage, skid marks, and anything else that’s relevant to how the accident played out.

- Write down your account of how the accident occurred.

- Get a full medical evaluation as soon as possible. Document medical treatment for any injuries sustained by you and your passengers.

- Report the accident to your insurance company, but stick to the basic facts. Don’t make statements like, “It was my fault” or “I wasn’t injured.”

- Consider hiring a Kern County personal injury lawyer for help in negotiating a fair settlement.

When you follow these steps after a car accident, you’re not only taking care of California’s legal reporting requirements and getting appropriate medical attention—you’re also starting to compile evidence to support your insurance claim or, if necessary, a lawsuit.

Understanding Pure Comparative Fault in California

In California, as in many other states, it matters who’s at fault in a car accident.

California applies a legal principle known as pure comparative fault to car accidents. Under pure comparative fault rules, you can collect damages in a car accident as long as you’re not completely at fault. Here’s how it works.

After a car accident, the insurance company—or a jury, if a case goes to trial—determines who is to blame for the crash. If a drunk driver loses control and hits another car, they’re likely to be declared 100% at fault. In many cases, however, responsibility for an accident isn’t as clear-cut.

For example, suppose a driver makes an illegal left turn in front of you and you crash into the side of their vehicle. Sounds like the other driver is at fault, right? But if it comes to light in the investigation that you were driving 10 miles per hour over the speed limit, the other driver’s insurance company might argue that you’re partially at fault—say, 10% responsible for the wreck. In that case, you can collect damages in proportion to the other driver’s percentage of fault. If you’re offered a $10,000 settlement, you would be able to collect 90% of it, or $9,000.

In theory, you can collect damages in California even if you’re 99% at fault in an accident, but such a scenario is very unlikely.

What Kinds of Damages Are Available in a Car Accident Settlement?

No discussion of the potential value of a claim for car accident damages is complete without mentioning the types of car accident damages available in California insurance claims and lawsuits. These damages fall into three categories:

- Economic damages are the simplest to calculate. They reimburse you for items such as:

- The cost of repairing your car (or the total value of your car if the cost of repairs is greater than the value of the car).

- Your medical expenses for treatment for car-accident-related injuries.

- Lost wages if you cannot work while you recover from your injuries.

- Future medical expenses if you have injuries that require ongoing or long-term treatment.

- Noneconomic damages don’t come with a specific dollar amount attached. They compensate you for intangible things like:

- Pain and suffering resulting from your injuries.

- Permanent disfigurement or disabilities resulting from your injuries.

- Loss of the enjoyment of life.

- Loss of the enjoyment of a relationship (such as a marriage; also known as loss of consortium).

- Punitive damages are rare. They are intended to punish defendants whose blatant negligence caused an accident.

In California, there is no statutory limit on noneconomic or punitive damages in car accident cases.

The Clock Is Ticking: Staying Within the Statute of Limitations

According to Section 335.1 of the California Code of Civil Procedure, a legal action for recovery of damages for a personal injury must be initiated within two years of the time of the injury in California.

Per Section 911.2 of the Government Code, personal injury claims against government entities in California must be filed within six months of the injury.

Note that these time limits apply to legal action—that is, lawsuits. Your car insurance company may require you to report a car accident within a certain (shorter) amount of time, so be sure to check the fine print on your insurance policy for specifics.

The primary takeaway is that you should initiate your insurance claim as soon as possible after an accident so the details of the crash are fresh and can be properly and thoroughly investigated.

Factors That Affect Car Accident Settlement Amounts

We can’t tell you that a California car accident claim with injuries will result in a settlement in a certain dollar range, but we can highlight factors that increase or decrease the average car accident settlement.

Some of these factors relate to the particulars of a crash—things that are out of your hands.

Others, however, involve the actions you take after an accident. In other words, what you do or don’t do could raise or lower your settlement amount.

Factors That Increase Compensation

Some factors increase the amount of car accident insurance settlements. These include:

- Property damage: In general, the greater the property damage, the greater the compensation.

- Injuries: Injury-causing accidents usually result in larger settlements. Typically, the more severe the injuries, the greater the compensation an insurer will offer.

- Third-party involvement: If an accident involves a third party, settlement amounts may increase substantially. For example, if a trucker rear-ends your vehicle, you may be able to file claims against the trucker and their employer.

- Business or government entity involvement: Businesses and government entities are likely to have more insurance coverage and more substantial assets. These factors may lead to larger settlements in such cases.

- Negligence: Cases involving a greater degree of negligence—for example, cases that involve reckless driving or driving under the influence of alcohol—may result in larger car insurance settlements.

The aforementioned factors relate strictly to the circumstances of an accident and are out of your control. However, the following actions may help increase your car insurance compensation:

- Fulfilling reporting requirements: Promptly taking care of reports to the police, the DMV, and the insurance company begins to build evidence for your claim.

- Getting eyewitness statements: Witnesses who testify to confirm that you weren’t at fault in an accident strengthen your claim for compensation.

- Documenting the crash and its aftermath: Recording the scene of the accident and vehicle damage with photos and videos and keeping all paperwork related to your medical examinations and treatment substantiates your demands for economic damages.

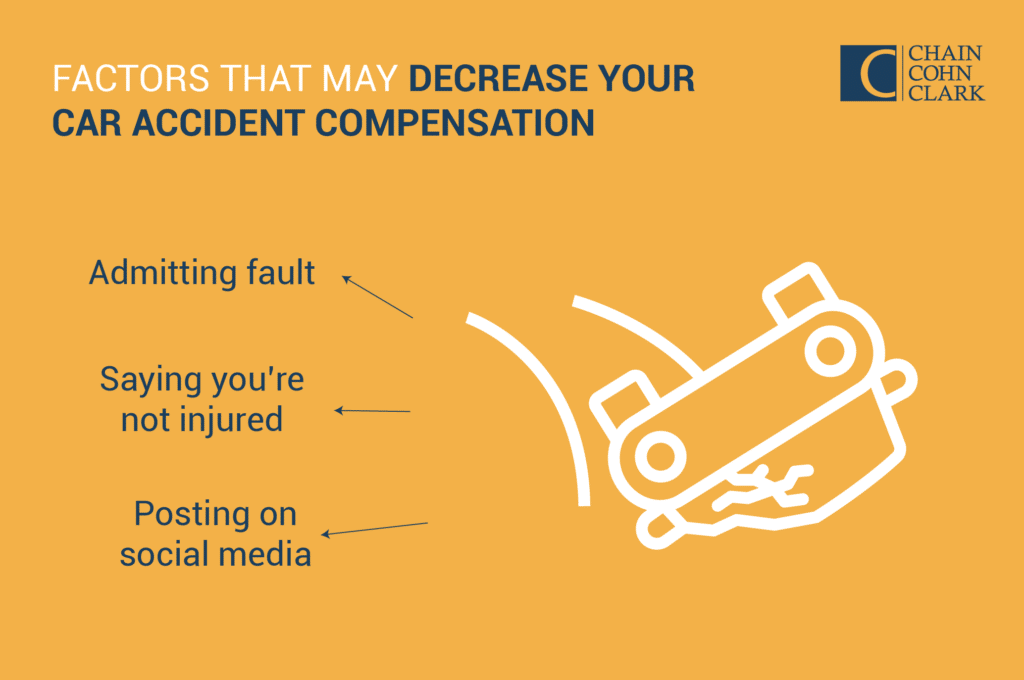

Factors That Decrease Compensation

One major factor that can decrease your insurance settlement is if you are partly to blame for the accident. Of course, this isn’t something you can change after a collision has occurred. But if you’re not careful, you may unwittingly do things that reduce the amount of any settlement you’re offered in a car accident case.

For example, you should avoid:

- Admitting fault: After an accident, suppose you say to the other driver, “I’m so sorry”—perhaps out of politeness. If this statement is reported to the other driver’s insurance company, they may use it to argue that you were at fault in the accident. When you speak to the police or insurance companies, stick to the facts of the accident and refrain from assuming blame—even partial blame—for what happened.

- Saying you’re not injured: Suppose that after an accident, you remark to the other driver, “I’m okay.” If you subsequently file a claim for compensation for medical expenses, the other driver’s insurance company may use what you said to argue that you weren’t injured. In truth, many injuries aren’t immediately obvious after a car accident. For example, you may not feel back or neck soreness due to whiplash until a day later.

- Posting on social media: As a rule of thumb, it’s wise to avoid any social media posts related to your car accident, because anything you say publicly about the accident can potentially be used in the other driver’s defense.

Another Factor Affecting Car Accident Settlements

One reason why it’s impossible to give a blanket estimate for the average amount of a car insurance claim is that claims vary from location to location. The cost of living—for instance, the cost of housing, food, utilities, and other necessities—varies from place to place. Car insurance rates vary from place to place, too.

Similarly, average California car insurance settlements differ from average settlement amounts in other states. Likewise, average Bakersfield car insurance settlements differ from average settlement amounts in other California cities.

Insurance Company Formulas for Estimating Damages

Economic damages are tied to specific dollar amounts, such as the cost of your car repairs or your doctor’s bills. Your insurer can calculate the amount of these damages simply by adding up the expenses or losses you’ve documented.

But noneconomic damages are more subjective; they require the insurance company or a jury to put a dollar amount on the pain or emotional distress your injuries have caused. Most insurance companies use a proprietary formula to calculate noneconomic damages, multiplying total economic damages by a factor between one and five based on the severity of your injuries and the evidence collected in the case.

Car Insurance Limits: A Potential Limit on Your California Car Accident Settlement

California currently requires minimum car insurance coverage as follows:

- Bodily injury liability coverage of $15,000 per person

- Bodily injury liability coverage of $30,000 per accident

- Property damage liability coverage of $5,000 per accident

For example, suppose you and a passenger are injured in a collision caused by a driver who’s carrying California’s minimum coverage limits. You have medical bills totaling $20,000, your passenger has medical bills of $30,000, and your car is beyond repair.

The most the at-fault driver’s insurance policy will pay for medical bills for the entire accident is $30,000; the most the policy will pay per person is $15,000. Therefore, if you’re offered a settlement for the full coverage amounts on the policy, you would have an additional $5,000 in unpaid medical bills, and your passenger would have an additional $15,000 in unpaid bills.

Your car is currently worth $30,000, but the at-fault driver’s policy will only pay $5,000—nowhere near enough to replace your car.

In a scenario like this, what are your options?

First, you could pursue a lawsuit against the at-fault driver. If they have assets, such as savings accounts or equity in a home they own, you may be able to secure a settlement or jury decision against them and make up the difference in your costs.

A second, simpler way to protect yourself against this kind of scenario is to purchase an adequate amount of uninsured/underinsured motorist (UM/UIM) coverage. UM/UIM coverage fills in gaps in coverage when the at-fault driver’s insurance is inadequate.

For example, suppose you have UM/UIM coverage of $100,000 per person and $300,000 per accident for bodily injury and $50,000 for property damage. In the previous scenario, your UM/UIM coverage would easily make up the gap in coverage and provide the additional $20,000 in medical bills and $25,000 in property damage—without the need for a lawsuit.

Experienced Bakersfield Car Accident Lawyers

If you were in a car accident caused by another driver, you’re entitled to a fair insurance settlement that compensates you for property damage, medical expenses, and your pain and suffering. But even if you do everything you should, you may not get a reasonable offer from the at-fault driver’s insurance company.

It’s no secret that people get larger car accident settlements when they have legal representation. The car accident attorneys at Chain | Cohn | Clark have the experience to evaluate the value of car accident insurance claims in Bakersfield and Kern County and can help you negotiate a settlement that meets your needs. And if negotiation doesn’t produce a suitable settlement offer, we’re prepared to take your case to court.

To learn what your car accident claim may be worth, contact Chain | Cohn | Clark today for a free, no-obligation case review.

Contact Us Today

for your free case evaluation

Fill out the simple form below and we’ll contact you about your case right away.